{kind=link}

By Lautaro Clavero, Student at the National University of Córdoba

In 1889, Otto von Bismarck implemented the pay-as-you-go pension system. The idea was promoted as a guarantee of social security that would protect workers in old age. However, when analyzing the demographic context of the time, it becomes clear that the promise of coverage was more symbolic than effective.

Of the 45 million inhabitants of the German Empire, only 7.9% were over the age of 60 (Kertzer & Laslett, 1995). Within this group, two-thirds were women, who did not receive direct pensions, except in some cases of widowhood. Meanwhile, the men who did receive pensions were those who had worked as formal industrial wage laborers, with a retirement age set at 70.

This meant that fewer than 0.5% of the population were actually covered by social security, while the industrial sector accounted for 14% of the population. In other words, for every pension beneficiary, there were approximately 28 contributors (German History in Documents and Images).

In practice, social security functioned as a tax on labor, due to the high contributor-to-beneficiary ratio. Bismarck, who may have been a poor demographer but was undoubtedly a shrewd politician, succeeded in marketing a concealed tax as a social benefit.

A more contemporary illustration of this conceptual ambiguity can be found in the case of the Amish in the United States, who refused to pay into the social security system. Their strict religious lifestyle permits them to pay taxes but prohibits them from purchasing insurance of any kind. They brought their case before the Supreme Court, which ruled that while the Amish could be exempted from certain insurance-based programs (such as Medicare), they were nonetheless required to contribute to social security, since it was not deemed an insurance scheme but rather a tax (Supreme Court, 1982).

Nevertheless, the system did begin to fulfill its intended function after the 1950s, when life expectancy in developed countries started to exceed 65 years, and old-age coverage became a significant public expenditure.

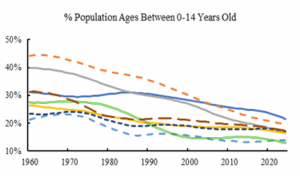

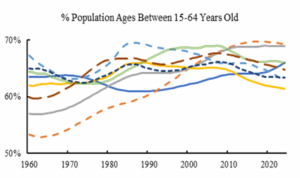

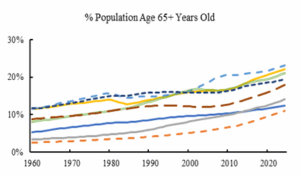

Despite this more effective functioning during the second half of the 20th century, the underlying design flaw remained; it was merely obscured by a demographic context that was far less critical than it is today. To illustrate this situation, one need only refer to Figure 1.

Figure 1: Changes in Population Structure by Age Group

Compiled by the author using World Bank data

Despite the heterogeneity among countries, all exhibit the same demographic trend: population aging coupled with a sharp decline in birth rates. It is this demographic transition that places the pension system under strain. A substantial increase in the number of pension beneficiaries, combined with a reduction in the number of contributors, puts the entire financial structure at risk.

It is evident that not all countries are affected in the same way, due to three key factors. First, although the overall trend is consistent, countries are at different stages of the demographic transition. For example, Brazil has less than half the proportion of people over 65 compared to Germany.

Second, more capitalized (developed) economies have greater room for maneuver in the face of rising social expenditures, owing to better access to credit and stronger fiscal capacity.

Third, not all countries employ the same type of social security system. Argentina and Brazil operate state-run pay-as-you-go contributory systems. France, Germany, and Spain also rely on contributory public pension schemes, but allow voluntary contributions to private capitalization systems. Chile, the United States, and the United Kingdom have mixed systems—that is, a combination of public pay-as-you-go mechanisms and privately managed funded schemes.

This last point lies at the heart of the current debate. The original pure pay-as-you-go model was bound to collapse from the outset, given the inevitable demographic evolution of modern societies.

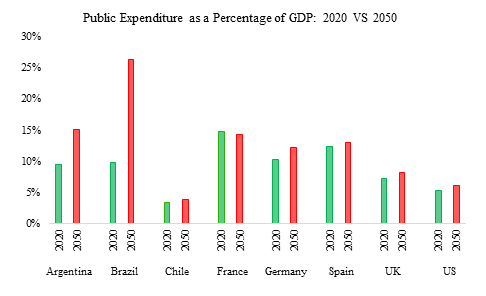

To better visualize this phenomenon, Figure 2 presents public pension expenditure in 2020 along with projections through 2050.

Figure 2: Public Funds Directed Toward the Financing of Retirement Pensions

Author’s own elaboration based on data from the OECD (Pensions at a Glance 2023) and ECLAC (Ageing in Latin America and the Caribbean)

The obvious conclusion is that countries relying solely on state-run pay-as-you-go systems will face the most significant increases in public spending. However, the data do not fully capture the underlying reality.

Not only will public expenditure rise—along with the associated increase in fiscal pressure—but this new contributory burden will fall on a shrinking labor force. This means that, if the current system is maintained, workers will be required to make higher contributions (in the form of taxes), thereby reducing their disposable income and, consequently, their capacity to save and consume.

Should the cost be shifted onto firms, the outcome remains unchanged. Higher corporate taxes undermine capital accumulation, which in turn affects labor productivity and thus real wages.

From the above, it follows that all countries will need to reconfigure their social protection systems—at least in relation to the pay-as-you-go component. Yet this is no easy task. Any adjustment to its three main variables—retirement age, contribution rate, or replacement rate—is politically unpopular, socially regressive, and ultimately temporary in effect.

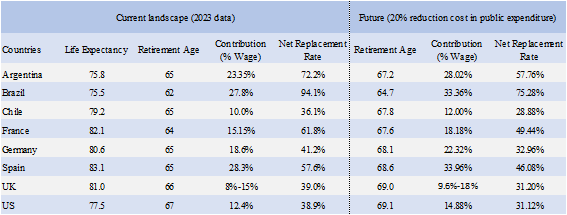

Table 1 presents both the current state of these variables across selected countries and a theoretical scenario showing how each would need to be adjusted in order to reduce the share of pensions in public expenditure by 20%.

Table 1: Present Indicators Versus Theoretical Adjustment

Author’s own elaboration based on data from the OECD, Pensions at a Glance 2023

Table 1 yields several important insights. Whether through an increase in the retirement age, higher contributions from workers and employers, or a reduction in the replacement rate (or a modest adjustment to each), the system would need to be corrected to mitigate the impact on public finances.

Some countries have already embarked on this unpopular path, and although such reforms are necessary, they remain insufficient. The issue lies not in financial parameters, but in the structural design of the system itself.

As a result, there are no political incentives to address the long-term problem. Any restructuring of the pay-as-you-go model is likely to be temporary—offering a brief reduction in the fiscal deficit at a high cost to workers. Meanwhile, the core problem remains unresolved.

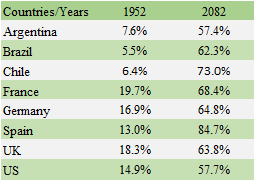

Table 2 presents the ratio of retirees to the economically active population, comparing data from 1952 with projections by the OECD for the year 2082.

Table 2: Percentage of Retirees Relative to the Economically Active Population

Author’s own elaboration based on data from the OECD, Pensions at a Glance 2023

Empirical evidence and projections reveal an uncomfortable truth: what was once a system designed to protect the elderly may now evolve into a profoundly unfair arrangement for today’s workers. New generations are contributing to a system that is structurally flawed—and from which they are unlikely to benefit.

This situation discourages workers from contributing to the system and motivates them to seek alternative mechanisms for social protection. After all, no one wants to pay into a system that will fail to support them when needed.

This dynamic fuels a vicious cycle in which current generations are increasingly unwilling to finance the retirement of previous ones, further weakening the system and reinforcing its dysfunction.

But then, is all hope lost?

Lautaro is a non-official ambassador of the Patagonia region where he was born. He is pursuing a bachelor’s degree in economics at Universidad Nacional de Córdoba. During 2021, he conducted his radio program, “La economía en una lección” (The Economy in One Lesson), while also starting to write as a journalist. His primary interests include macroeconomics and statistics, and he serves as a teaching assistant for these subjects at his university.